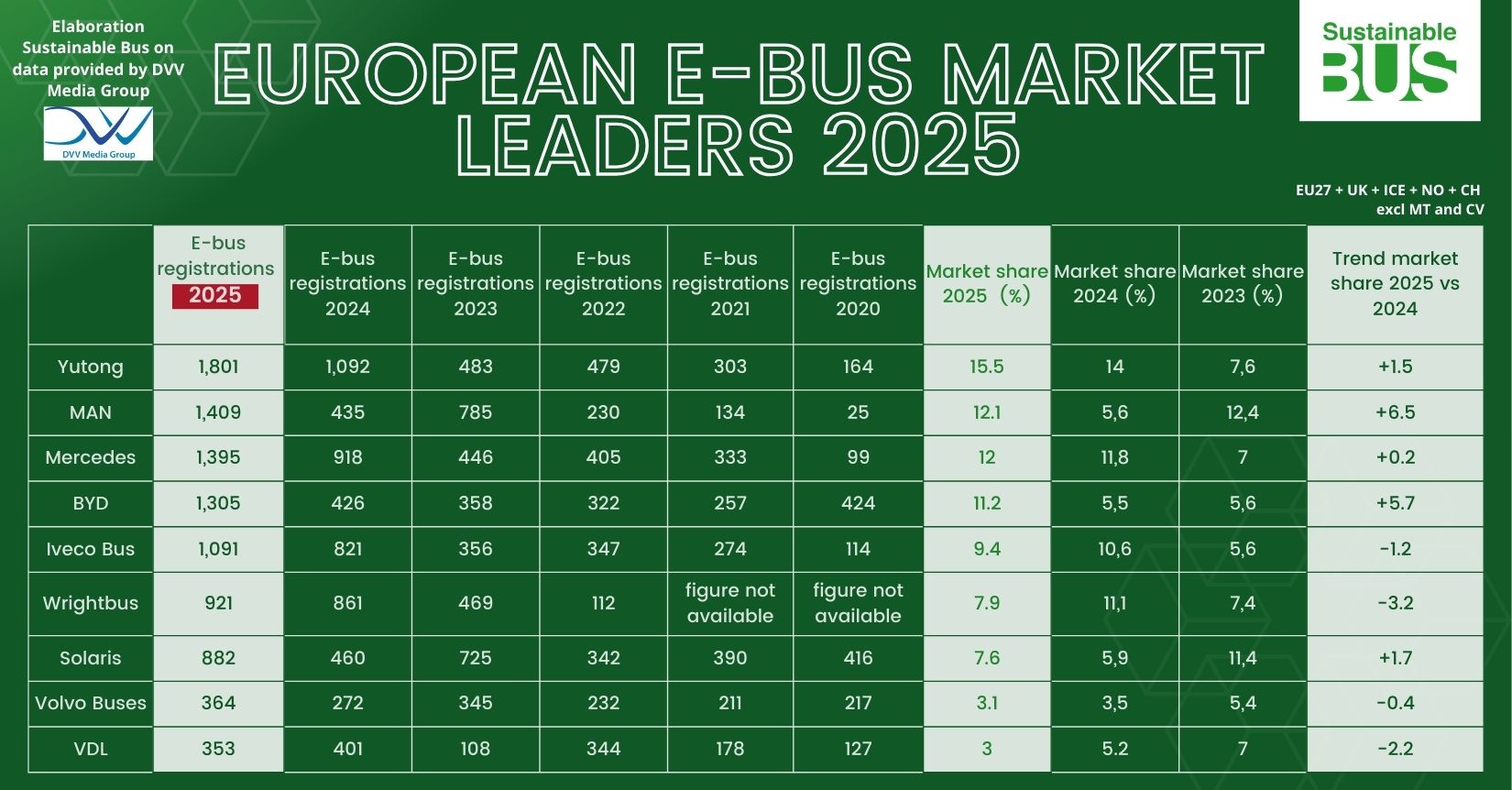

European electric bus market grew nearly 50% to 11,607 units in 2025 as MAN and BYD more than triple volumes

Electric bus registrations in Europe reached 11,607 units in 2025 for vehicles above 8 tonnes GVW, representing a +48% on the 7,855 registered in 2024. MAN and BYD recorded the strongest increases among major manufacturers in 2025, with registrations rising to 1,409 units for MAN (+224%) and 1,305 units for BYD (+206%), both gaining significant […]

Electric bus registrations in Europe reached 11,607 units in 2025 for vehicles above 8 tonnes GVW, representing a +48% on the 7,855 registered in 2024.

MAN and BYD recorded the strongest increases among major manufacturers in 2025, with registrations rising to 1,409 units for MAN (+224%) and 1,305 units for BYD (+206%), both gaining significant market share. Mercedes also expanded volumes to 1,395 electric buses (+52%), maintaining a broadly stable market share around 12%.

The dataset covers the markets of EU27 together with the United Kingdom, Iceland, Norway, Switzerland, Serbia and Ukraine and excludes trolleybuses. The figures are compiled from national statistics bodies and included in the 2025 Annual Report on European Bus Data released by DVV Media Group.

Zero-emission buses reached 60% of EU city bus market in 2025, while one quarter of the total market (then including coaches) was covered by ‘electrically-chargeable’ buses.

Registrations had reached 7,855 units in 2024, growing 22% compared with 2023. The momentum continued into the following year: more than 8,000 electric buses were already registered between January and September.

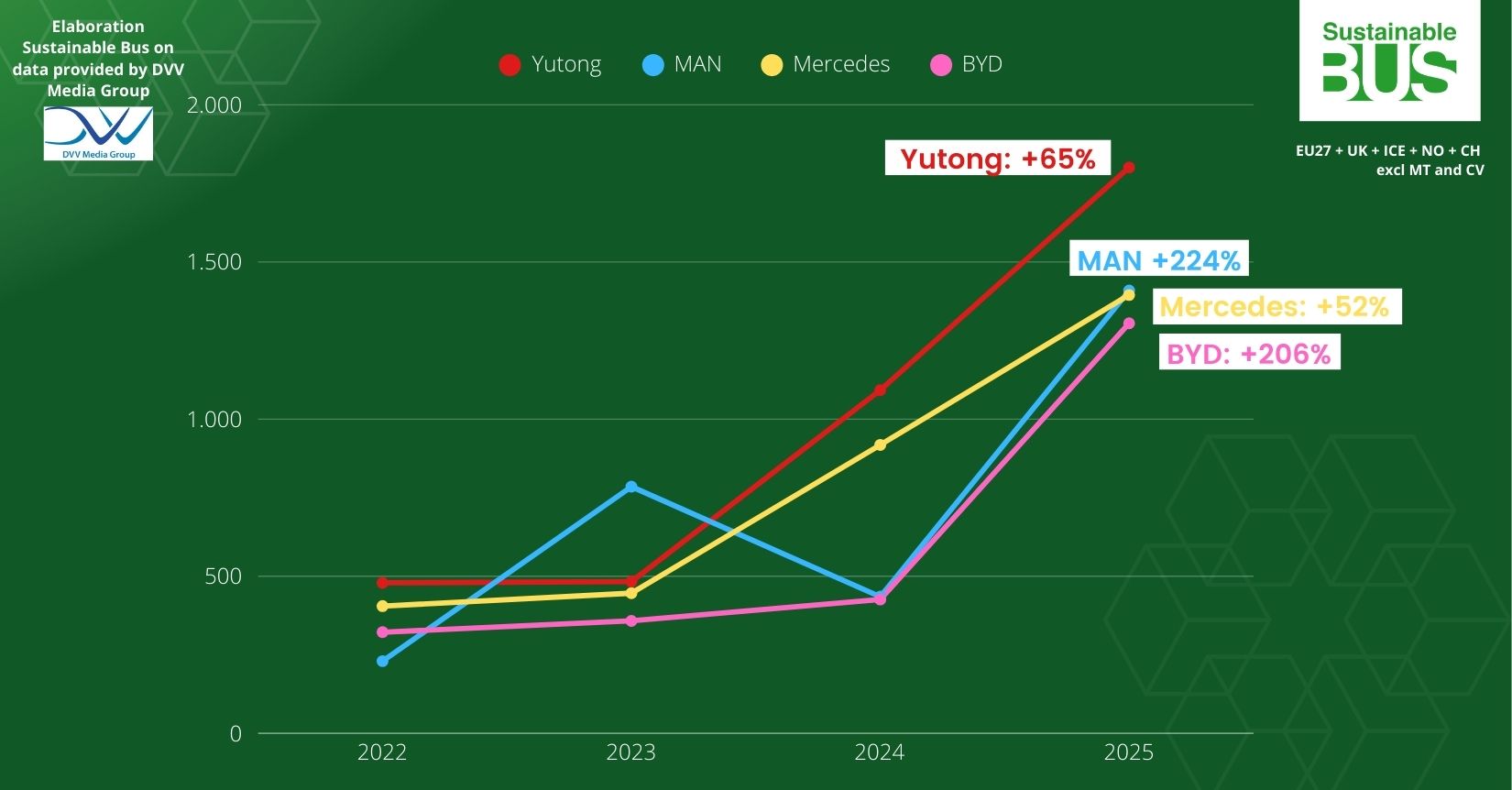

Yutong remains market leader as MAN and BYD expand volumes

Yutong retained the leading position in the European electric bus market with 1,801 registrations, increasing from 1,092 units in 2024. The manufacturer expanded its market share from 14.0% to 15.5%, consolidating its lead. The most significant shift in the ranking comes from MAN, whose registrations rose from 435 units in 2024 to 1,409 in 2025, representing +224% growth. This increase lifted the manufacturer’s market share from 5.6% to 12.1%, moving it into second position in the European market.

Daimler Buses recorded 1,395 registrations, up from 918 units in 2024 (+52%). Its market share remained broadly stable at around 12%, moving from 11.8% to 12.0%.

BYD posted one of the strongest increases in the market, with registrations rising from 426 units to 1,305 buses (+206%). As a result, its market share expanded from 5.5% to 11.2%, bringing the manufacturer close to the top tier of the ranking. These four manufacturers, all together, made half of the European e-bus market last year.

Mixed developments among other major manufacturers

Iveco Bus increased registrations to 1,091 units (from 821 in 2024, +33%), although its market share declined from 10.6% to 9.4%. Wrightbus recorded 921 buses, slightly above 861 units in 2024, but its share dropped more significantly from 11.1% to 7.9% as the overall market expanded. Solaris posted one of the strongest increases in the segment, with registrations rising from 460 to 882 buses (+92%), lifting its market share from 5.9% to 7.6%. Volvo Buses also increased volumes to 364 units (+34% from 272 in 2024), while its share edged down from 3.5% to 3.1%. In contrast, VDL Bus & Coach recorded 353 registrations, declining from 401 units in 2024 (-12%), with market share falling from 5.2% to 3.0%.

Among smaller-volume manufacturers, Karsan increased registrations from 171 to 313 buses (+83%), raising its share from 2.2% to 2.7%, while Alexander Dennis grew from 165 to 298 units (+81%), expanding its market share from 2.1% to 2.6%.

In contrast, Irizar recorded 211 registrations, down from 263 units in 2024 (-20%), with market share decreasing from 3.4% to 1.8%. Ebusco registered 122 electric buses, compared with 151 units in 2024.

Hydrogen buses: 558 registrations in 2025

Hydrogen fuel-cell buses accounted for 558 registrations in 2025 across the European markets included in the DVV dataset. Solaris represents the largest manufacturer with 277 units, corresponding to 49.6% of the segment, followed by Wrightbus with 95 buses and Mercedes with 85 units. By country, Germany accounts for the largest share of the hydrogen bus market with 336 registrations, representing 60.2% of the total, followed by France with 47 buses, Italy with 36, and Poland with 35.

Intercity buses and coaches?

What is interesting, registrations of alternative driveline intercity buses reached 2,881 units in 2025. Hybrid buses represent the largest share with 1,134 units, followed by 1,157 CNG buses, while 590 battery-electric intercity buses were registered during the year. In the coach segment, volumes remain comparatively small. The dataset reports 390 non-diesel coaches in 2025, including 267 electric coaches, 111 CNG models, and 12 hybrid vehicles.

Evolution of alternative driveline buses in Europe

Still according to DVV figures, total registrations of non-diesel buses above 8 tonnes reached 17,108 units in 2025, compared with 14,417 in 2024. Battery-electric buses represent the largest segment with 11,607 registrations, followed by 2,565 hybrid buses, 2,378 CNG buses, and 558 fuel cell buses. Looking at a broader time frame, electric buses increased from 101 units in 2015 to 11,607 in 2025, while hybrid and CNG buses show lower volumes in recent years compared with their peaks earlier in the decade.