EU zero-emission bus registrations made 24% of the market in Q1 2026, says ICCT. Top sellers? Yutong, Solaris, MAN

EU zero-emission bus and coach registrations reached 24.2% of the market in the first quarter of 2026, with 2,732 vehicles sold across the European Union, according to the latest quarterly market monitor published by the International Council on Clean Transportation (ICCT). Bus and coach registrations above 3.5 tonnes totaled 11,300 units in the EU between […]

EU zero-emission bus and coach registrations reached 24.2% of the market in the first quarter of 2026, with 2,732 vehicles sold across the European Union, according to the latest quarterly market monitor published by the International Council on Clean Transportation (ICCT).

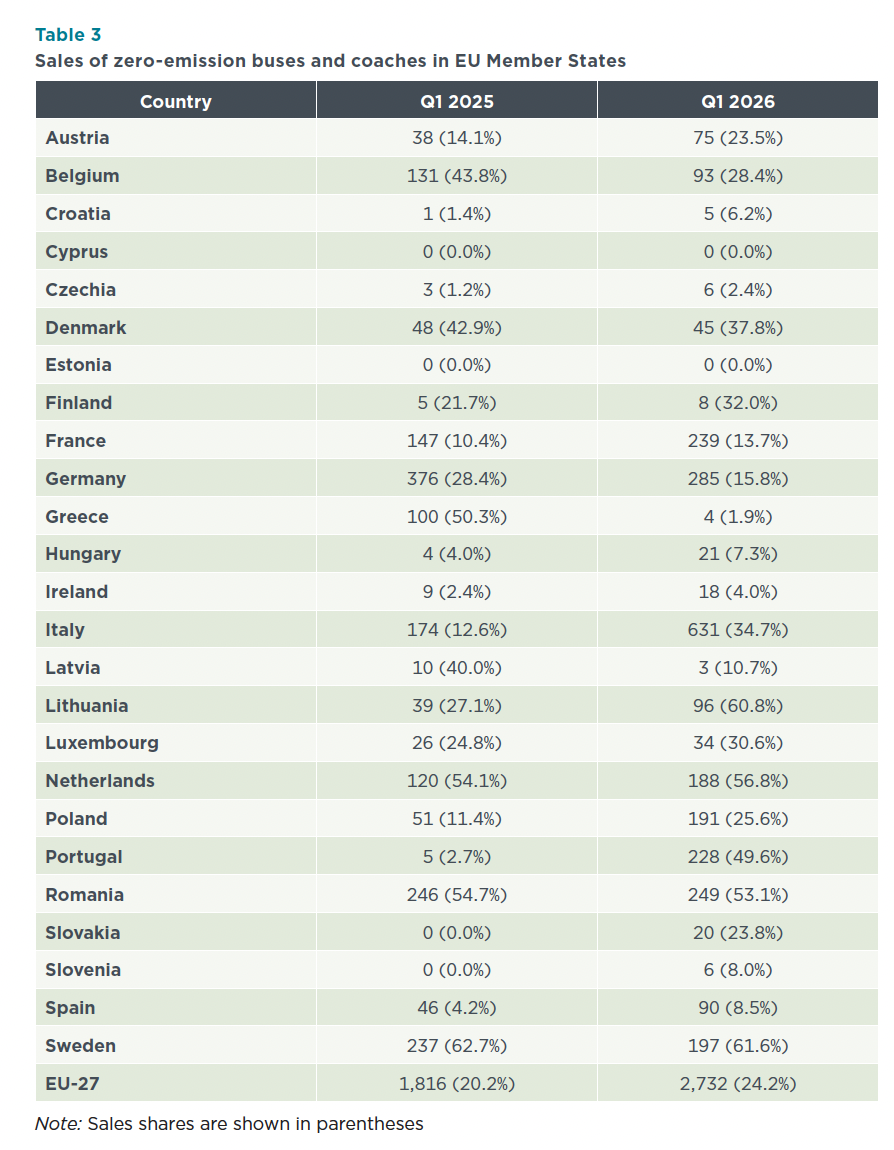

Bus and coach registrations above 3.5 tonnes totaled 11,300 units in the EU between January and March, with zero-emission vehicles accounting for 2,732 registrations, corresponding to a 24.2% market share. The figure compares with 1,816 units and a 20.2% share recorded in the first quarter of 2025. The 24% share of e-buses is aligned to the market share found by ACEA in 2025.

The bus segment recorded the highest zero-emission penetration among all heavy-duty vehicle categories covered in the report. Across the broader heavy-duty vehicle market, zero-emission trucks above 3.5 tonnes reached a 4.5%.

According to the just-released BloombergNEF’s Electric Vehicle Outlook 2026, on a global scale, more than 20 countries surpassed 50% electric city bus sales in 2025 as e-buses head for 60% of global market by 2030.

EU bus market reaches 2,732 zero-emission registrations

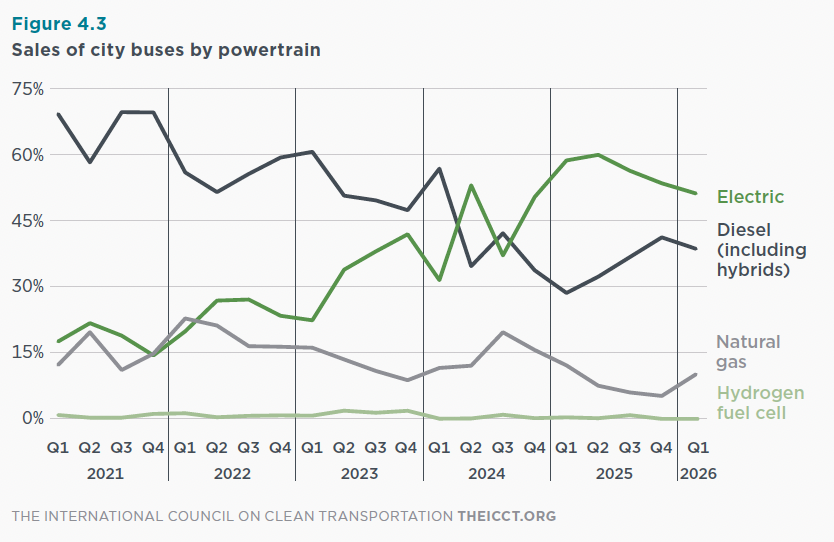

ICCT data show that battery-electric technology remained the dominant zero-emission solution in the urban bus segment. Among city buses registered in Q1 2026, battery-electric models represented 55% of sales, while diesel and diesel-hybrid vehicles accounted for 36% and natural gas for 9%. In the interurban bus and coach category, diesel retained a 92% share, with battery-electric vehicles at 5% and natural gas at 3%. Minibuses registered a 13% battery-electric share.

Historic market data presented by ICCT indicate that annual EU zero-emission bus and coach registrations increased from approximately 1,700 units in 2020 to 9,800 units in 2025. In the first quarter comparison, registrations rose from 1,900 units in Q1 2025 to 2,700 units in Q1 2026, while market share increased from 20% to 24%.

The report highlights substantial differences between national markets. Sweden recorded the highest share among major mature markets with 197 zero-emission bus and coach registrations and a 61.6% share. The Netherlands reached 188 units and a 56.8% share, while Romania registered 249 vehicles corresponding to a 53.1% share. Lithuania posted the highest share among larger growth markets at 60.8%, with 96 registrations.

Italy leads volume growth

Italy registered the largest year-on-year increase in absolute volumes among EU Member States. Zero-emission bus and coach registrations rose from 174 units in Q1 2025 to 631 units in Q1 2026, increasing market share from 12.6% to 34.7%. Portugal recorded 228 registrations and a 49.6% share, compared with five vehicles and a 2.7% share in the corresponding period of 2025. Poland increased from 51 to 191 units, reaching a 25.6% market share.

In brief

- What was the EU zero-emission bus and coach market share in Q1 2026?

24.2%, corresponding to 2,732 registrations out of approximately 11,300 buses and coaches sold. - Which country registered the largest number of additional zero-emission buses?

Italy, with registrations increasing from 174 units in Q1 2025 to 631 units in Q1 2026. - What share did battery-electric city buses achieve?

Battery-electric buses accounted for 55% of EU city bus registrations in Q1 2026. - Which manufacturer led zero-emission bus sales share?

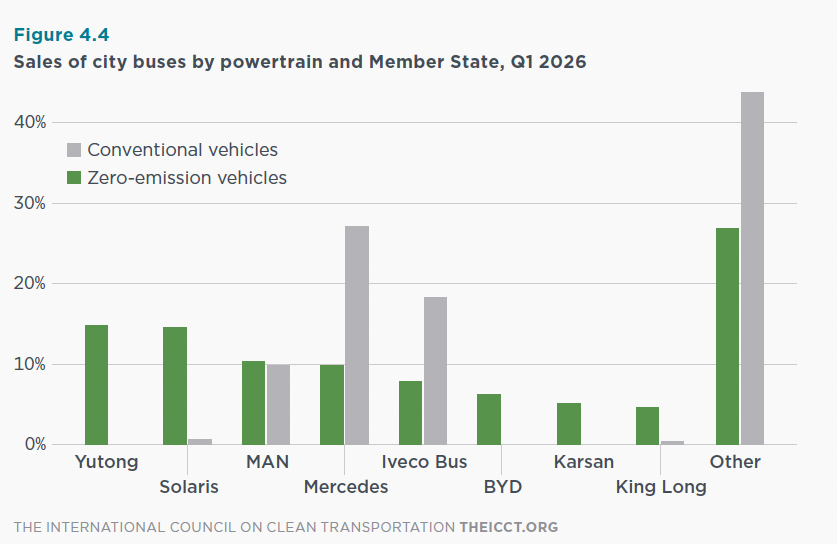

According to ICCT, Yutong recorded the highest zero-emission bus sales share in Q1 2026. Solaris followed closely, while MAN exceeded 10%. Iveco Bus held close to 8%.

France recorded 239 zero-emission bus and coach registrations, representing 13.7% of the national market, compared with 147 units and 10.4% one year earlier. Germany registered 285 units and a 15.8% share, compared with 376 units and 28.4% in Q1 2025. Belgium moved from 43.8% to 28.4%, while Greece declined from 50.3% to 1.9%.

Yutong ranks first among manufacturers

The manufacturer breakdown of zero-emission city bus registrations showed a diversified competitive landscape in Q1 2026. According to ICCT data, Yutong recorded the highest share of zero-emission city bus sales, accounting for nearly 15% of all zero-emission city bus registrations in the EU. Solaris followed closely, while MAN exceeded 10%. Iveco Bus held close to 8% of zero-emission city bus registrations, ahead of BYD at around 6%, Karsan at approximately 5%, and King Long at nearly 5%.

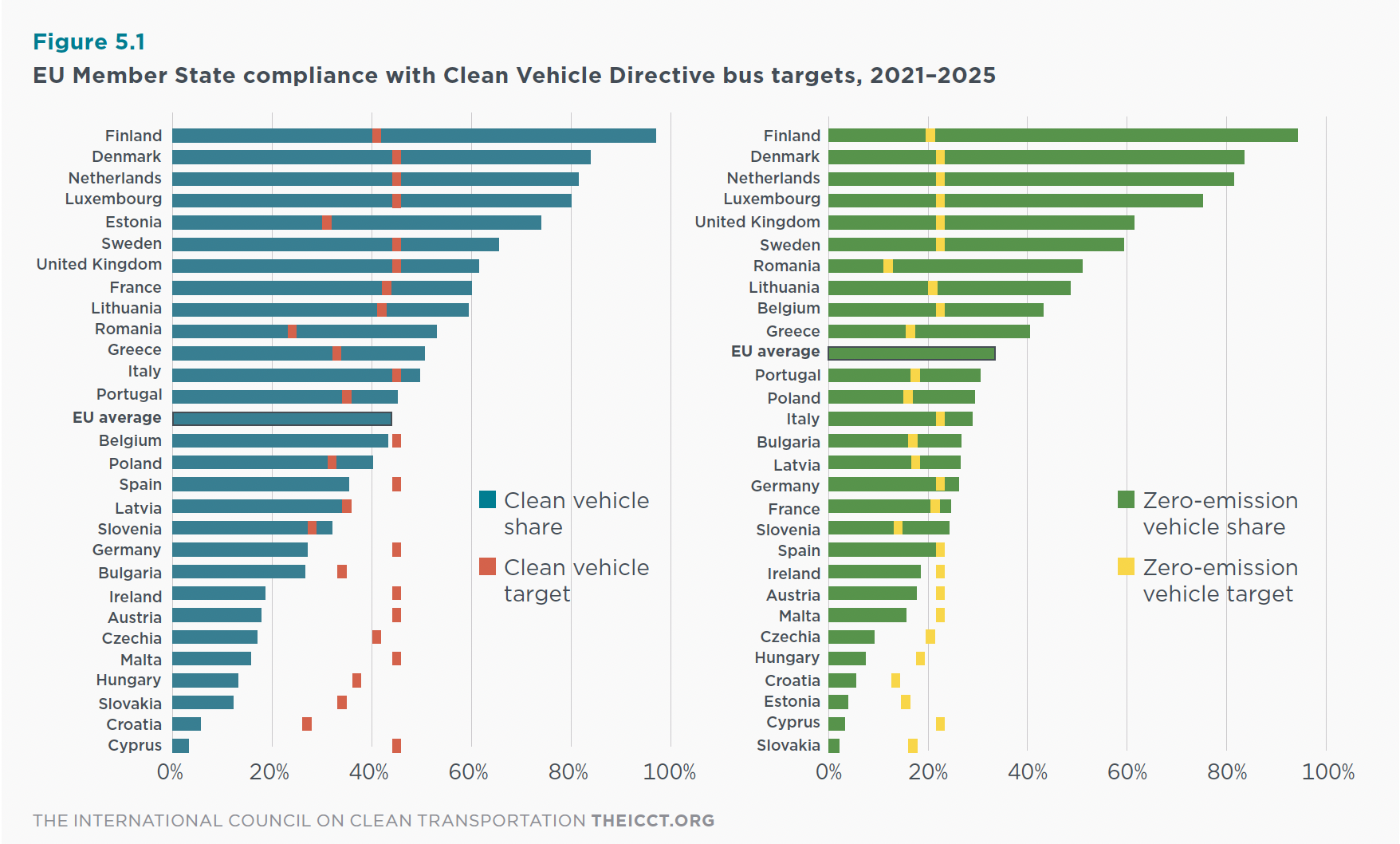

The report dedicates a section to the implementation of the Clean Vehicle Directive. According to ICCT calculations, 18 EU Member States achieved their zero-emission bus procurement targets during the 2021–2025 reporting period, while 15 met their broader clean vehicle targets. As of 2026, higher public procurement requirements for zero-emission buses entered into force under the second phase of the Clean Vehicle Directive, covering the period 2026–2030.